The headline video is a summary of below and focuses on the Q&A portion of the presser.

Sources for my analysis:

The Video itself

Peter Schiff.

My Brain… human summary by me:

The Fed is being disingenuous about inflation. It is raging as I have been saying all along. The way they calculate inflation between now and 1970s has changed on purpose to promote business confidence

They cannot raise rates even if they want to because of all the debt in the system. The only way they can truly fight inflation by raising rates high enough is AFTER collapse of the economy and stocks. When the pain is so great, everyone begs the government to raise rates to kill inflation

Paul Volcker didn’t prevent inflation…He fought raging inflation after he was given permission to fight it.

So the Fed can still monetize the debt through their back channel operations, but the only sledgehammers they have now are 1) Not cutting is the new raising and 2) cut rates and cause more inflation

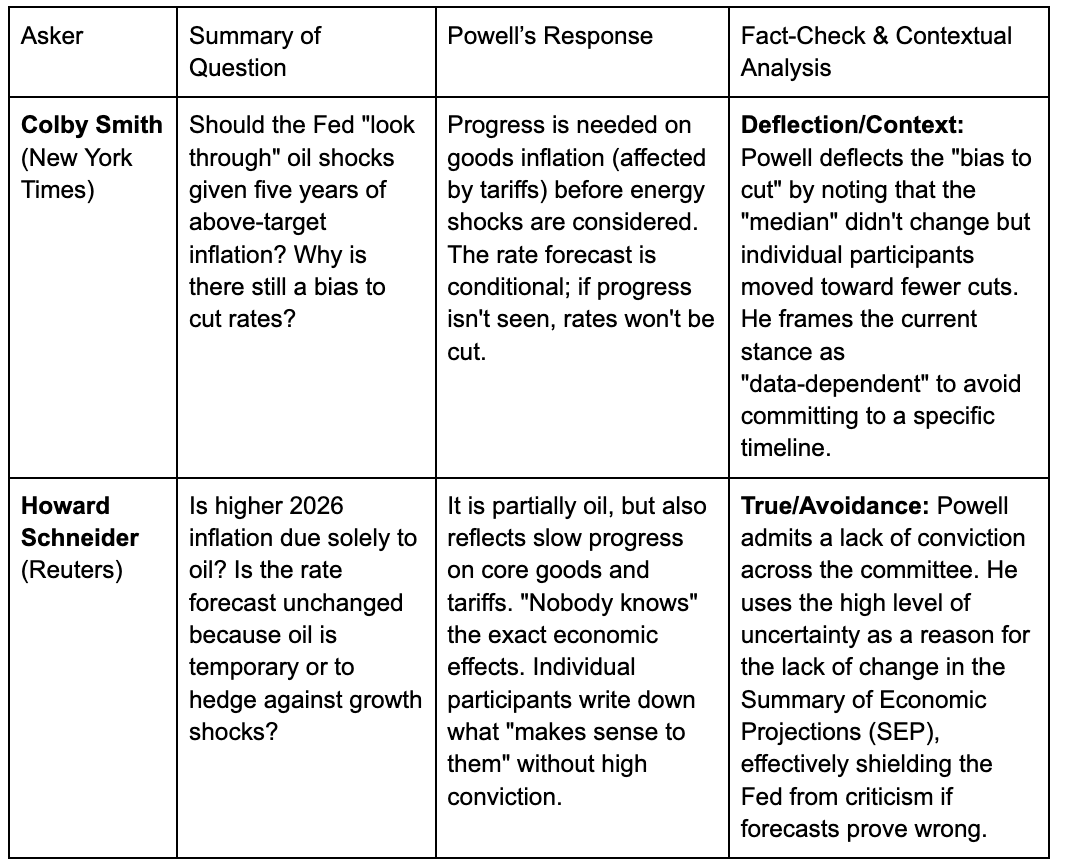

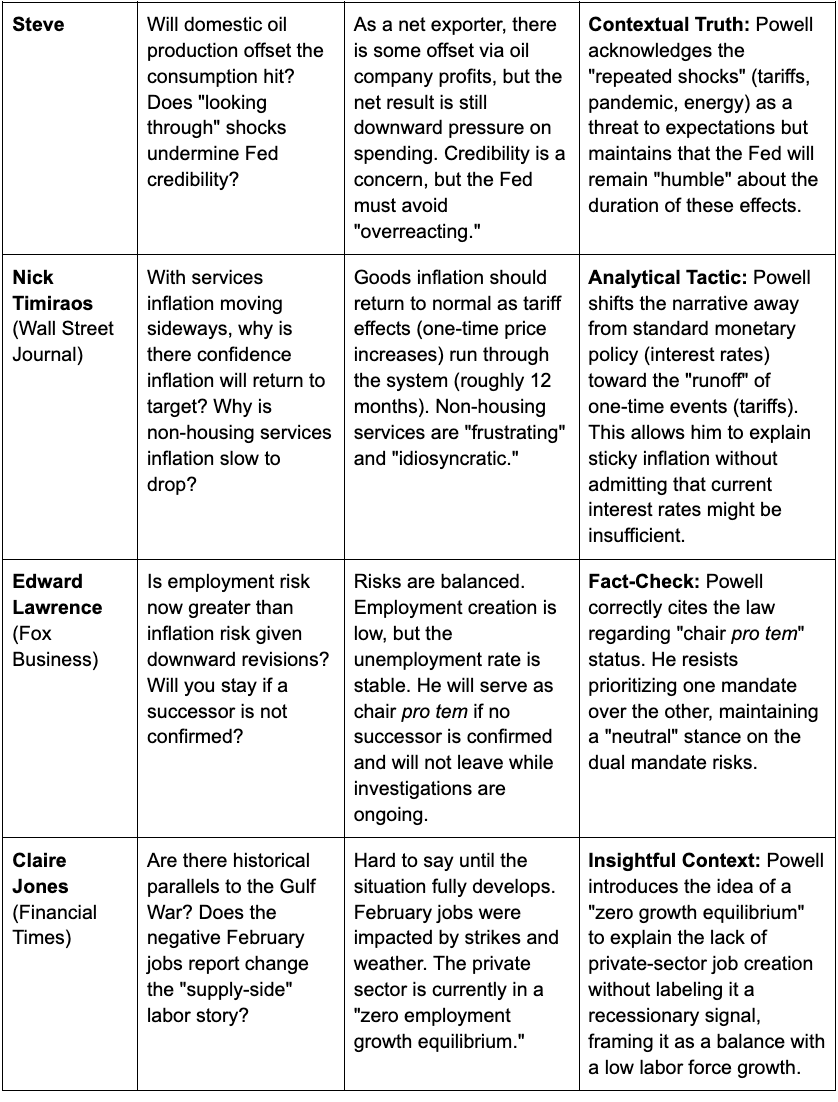

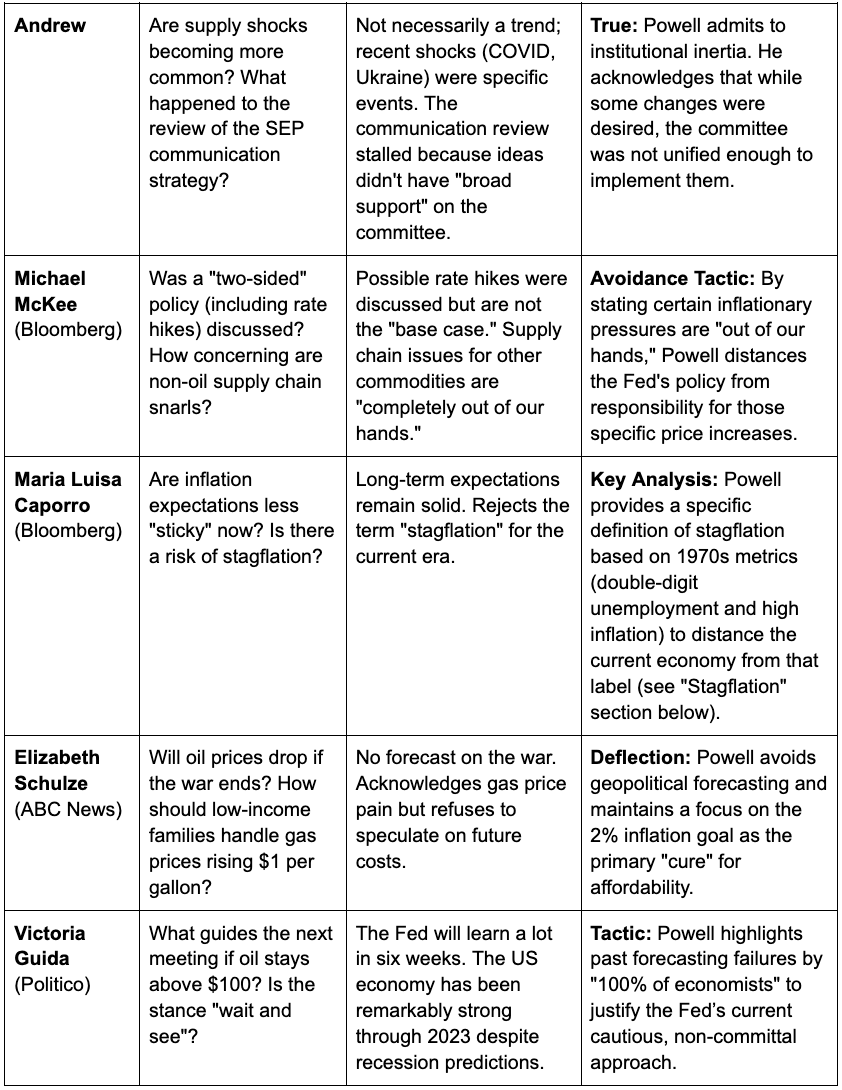

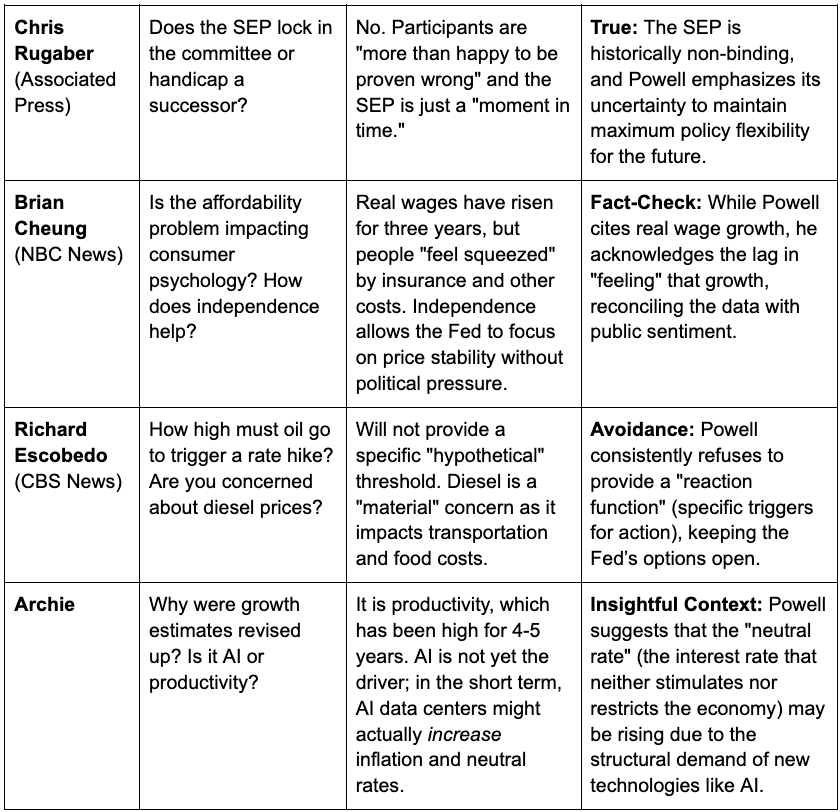

Below is a detailed summary using AI of each question, by whom, the reply by Powell and some fact checking.

Federal Reserve Press Conference: Q&A Analysis and Briefing

This briefing document provides a comprehensive synthesis of the Question and Answer session following the Federal Reserve’s decision to maintain the federal funds rate. It details the inquiries from various news organizations, the responses provided by Chair Jerome Powell, and an analytical assessment of those responses for factual accuracy, context, and rhetorical tactics.

Q&A Session Analysis

Detailed Focus: Stagflation and Inflation Definitions

A significant portion of the Q&A focused on whether the US economy is entering a period of “stagflation”—a combination of stagnant economic growth and high inflation.

Powell’s Definition vs. Historical Context

Chair Powell explicitly rejected the “stagflation” label for the current economic environment. He argued that the term is reserved for the extreme conditions of the 1970s, characterized by:

Double-digit unemployment.

Extremely high inflation.

A very high “Misery Index” (the sum of the unemployment and inflation rates).

Powell’s Argument: He contrasted the 1970s with current data:

Unemployment: 4.4% (near longer-run normal).

Inflation: Approximately 3% (one percentage point above target).

Growth: Real GDP projected at 2.4%.

Powell concluded that while there is “tension” between the goals of maximum employment and stable prices, the situation is “nothing like what they faced in the 1970s.”

Fact-Check: Calculations Then vs. Now

While Powell focused on the levels of the indicators, he did not address the methodological changes in how inflation and stagflation are calculated today compared to the 1970s.

Inflation Calculation Shifts: In the 1970s, the Consumer Price Index (CPI) directly factored in home prices and mortgage interest rates. Today, the Fed prefers the Personal Consumption Expenditures (PCE) price index, and the CPI now uses “Owners’ Equivalent Rent,” which can smooth out housing volatility.

Stagflation Thresholds: Because the methodology for measuring inflation has changed (generally resulting in lower reported figures today for the same level of price increases), a 3% inflation rate today might represent more significant price pressure than a 3% rate in the 1970s.

The Misery Index: Powell used the “Misery Index” as his primary defense. However, critics argue that because the “natural rate of unemployment” and the calculation of “labor force participation” have shifted, a 4.4% unemployment rate today does not carry the same economic weight as it did in the 1970s.

Conclusion on Stagflation: Powell’s rejection of the term relies on a “severity-based” definition. By anchoring the definition of stagflation to the extreme outliers of the 1970s, he successfully avoids the label, even if the trend of slowing growth and elevated inflation is present.

--------------------------------------------------------------------------------

Key Insight: The “Tariff Runoff” Narrative

Throughout the briefing, Powell repeatedly pointed to tariffs as a primary driver of goods inflation. He categorized these as “one-time price increases” rather than “ongoing inflation.”

The Logic: A tariff raises the price of a good once. It creates a year-over-year inflation spike, but once that year passes, the effect drops out of the calculation.

The Strategy: By blaming tariffs for the “overshoot” in inflation, Powell provides the Fed with a reason to maintain current rates (or eventually cut them) without having to wait for interest rates to “break” the economy. He is effectively waiting for the “clock to run out” on the tariff price hikes.

The Risk: Powell admitted he is “uncertain” and “not certain” about how long it takes for these costs to work through the economy. If these “one-time” increases lead to higher inflation expectations, the “looking through” strategy could fail.