The above video with slides is a summary of a well crafted YouTube video by Sachs Realty on the dangerous setup in the housing market today.

The runtime is over 1 hour so I thought I would offer both the original source content and the AI summary

Housing Market Briefing: Cracks Are Showing – A Looming Implosion?

Executive Summary:

This briefing analyzes a recent discussion on the current state of the U.S. housing market, highlighting an underlying crisis of hidden foreclosures, government manipulation, and an impending affordability and economic downturn. While official narratives suggest a stable or improving market, the experts interviewed, a real estate broker specializing in foreclosures (John Hoffman) and a real estate educator (Todd), argue that "the whole thing is a gigantic mess" and "pain is coming right now." They predict a significant market correction, potentially leading to an "implosion" similar to or even exceeding the 2008 crisis, but with the added layer of hidden systemic issues.

Main Themes and Key Insights:

1. Hidden Foreclosures and Government "Fraud":

The most critical and alarming theme is the deliberate concealment of foreclosures, primarily through government-backed loans (FHA, VA, Fannie Mae, Freddie Mac).

"Masterfully Hidden" Foreclosures: "The foreclosures have been masterfully hidden." This is achieved through repeated "equity loans" or "workouts" for delinquent borrowers, pushing their debt to the back of the loan with "no interest" and "no paperwork."

Government as "The Fraud": The speakers explicitly state, "if you want to call it fraud but it's it's really it's the government They're the fraud." They describe how FHA and VA loans are being constantly modified, with the government essentially paying servicers to keep borrowers in their homes, even if they can't afford it.

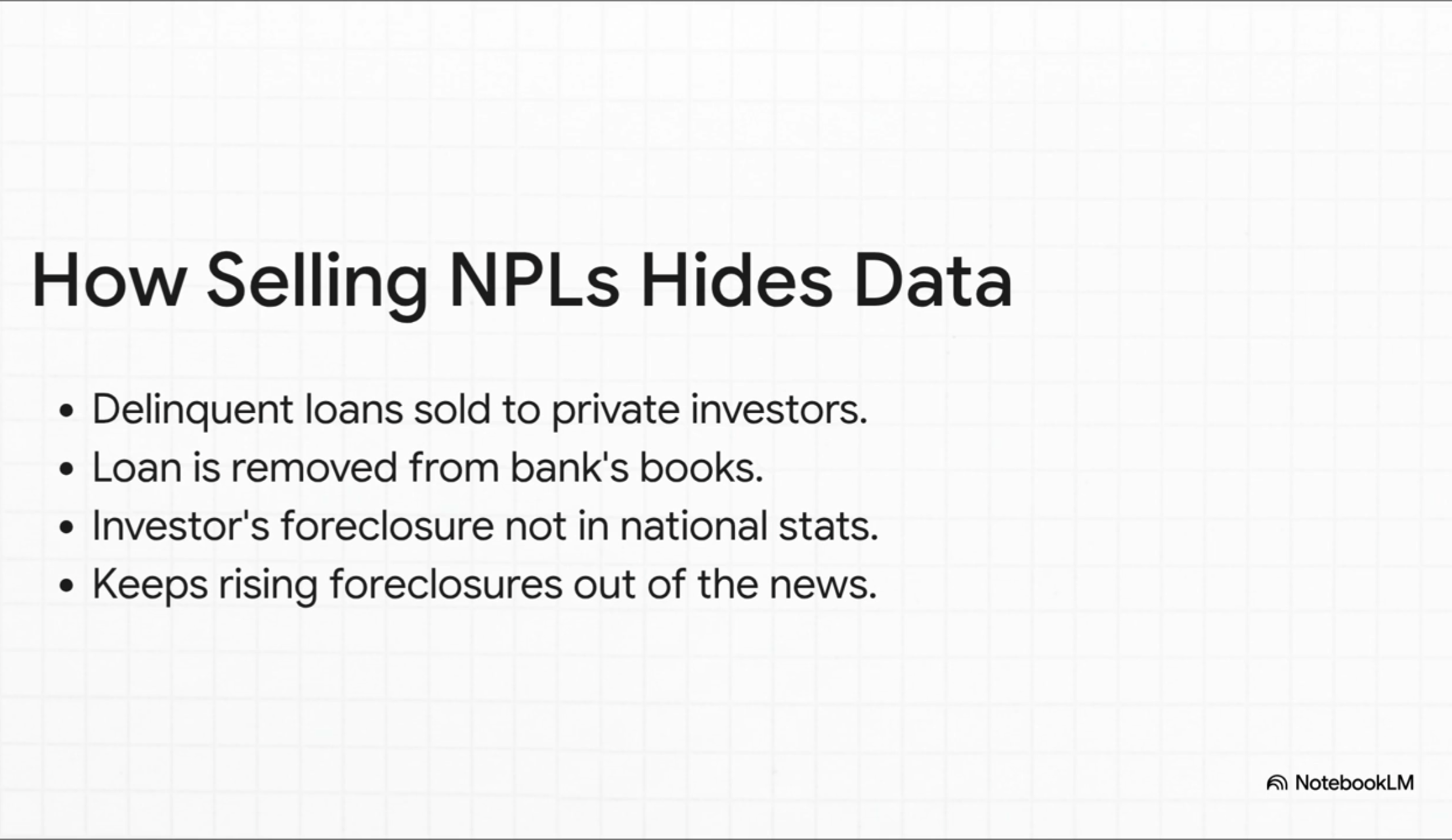

Pooling and Selling Delinquent Loans (NPLs and RPLs): Fannie Mae and Freddie Mac are "bundling these loans and selling them to Wall Street investors" as "non-performing loans (NPLs) and reperforming loans (RPLs)." This practice allows them to remove these distressed assets from their books, making it appear as if foreclosures are low and avoiding negative headlines. "They don't see they'd rather have somebody else foreclose on it That way it's not in the news that they're the bad guy."

Silent Foreclosures: Investors buying these pooled loans are not benevolent; they intend to profit. While required to honor existing modifications initially, the expectation is that they will quickly move to eviction if payments aren't made. This leads to a "silent 2008" where actual foreclosures are happening but are not publicly visible as "REOs" (Real Estate Owned by the bank). "You won't be able to see in headline news foreclosures are on the rise because this is the 27th sale they're announcing of bundles of mortgages."

Delinquency Rates in FHA/VA Loans: Data from specific Illinois districts shows FHA/VA loan delinquencies ranging from 15% to 24% (defined as two or more workouts). This indicates a significant portion of these government-backed loans are in trouble. "Anywhere from one in four one in five and and what you're showing here of these FHA I mean that's huge Or delinquent And these would be foreclosures."

Impact of Equity: The current high levels of home equity are the only thing sustaining this system. "as long as there's equity they're giving it to him anyways." However, "when home prices continue to go down the equity is not there any longer."

2. Affordability Crisis and Declining Market Conditions:

Despite some regions remaining "hot," the overall market is showing significant signs of cooling and an acute affordability crisis.

Cracks are Starting to Show: "right now all the cracks are starting to show." This includes "longer market times," "more stuff coming on the market," and "deals falling apart."

Buyers Getting Savvy: Buyers are "not buying this this this program anymore." Home inspections are leading to contract cancellations as buyers realize they've "overpaid." "We did our home inspection We're out."

Interest Rates vs. Affordability: The prevailing belief that lower Fed rates will revive the housing market is dismissed as "clueless." The speakers argue that mortgage rates don't directly follow Fed rate cuts (citing a September drop where mortgage rates rose) and that even significantly lower rates won't solve the fundamental affordability issue. "It would need to be in my opinion lower than 4% which I just don't see But what do you think is going to happen over the next 12 to 18 months with home prices coming down even by mean Northeast even Even there it's coming down There's no you you just you you can't maintain this."

High Prices as the Core Problem: The "elephant in the room" is "these ridiculous prices." Even with historically low rates, people cannot afford current home values, which also drive up property taxes and insurance. "The prices have to come down Everybody wants to talk about not talk about the all in the room which is these ridiculous prices."

Stagnant Market: The market is described as a "stagnant world until rates come down" by one interviewed attorney, but the hosts counter that even rate cuts won't fix the overvaluation.

Rehabbers and Investors: Local rehabbers are now "buying to rent" rather than flipping, and "lowballing stuff right now because they know these prices are not... recapturing what they want." Institutional buyers like American Homes for Rent are no longer actively acquiring properties.

Increased Inventory and Slow Showings: There's a noticeable increase in reactivated listings and "ghost town" showings for new properties, indicating a significant drop in buyer demand.

3. Broader Economic Concerns and Job Market Manipulation:

The housing market issues are interconnected with a broader, manipulated economic picture.

Bogus Job Numbers: The official job numbers are labeled "bogus," with consistent downward revisions and questions about their accuracy. "Trump has... a heart attack because these numbers are all bogus which they are."

Corporate Layoffs and Shareholder Focus: Large companies like Kroger are cutting "corporate jobs" not because their digital divisions are performing poorly, but to "show good numbers" to shareholders. This indicates a focus on maintaining stock prices over employment stability for higher-paid positions.

Consumer Strain: Families are struggling with grocery costs ($400/week for a family of four), and people are scrutinizing subscriptions, indicating a tightening of household budgets. "All you have to do is look at your own checkbook look at your you know your in your pocket Look at how expensive things cost."

California Law to Halt Second Mortgage Foreclosures: A proposed California bill to "halt second ... mortgage foreclosures" is viewed as another attempt by the government to hide problems and prevent negative headlines, ultimately being paid for by taxpayers. "What's what's our ultimate goal with this to keep it keep the blood off their hands keep it out of the you know no we don't whatever reason 08 in 08 whenever you know obviously everything went haywire Foreclosures everywhere Okay And now we're so far off on the other end that now we're not going to have any and we'll just figure out a way to hide these and the government can pay for them."

4. Timing of the Implosion:

The experts predict that the full impact of these hidden issues will become apparent in the near future.

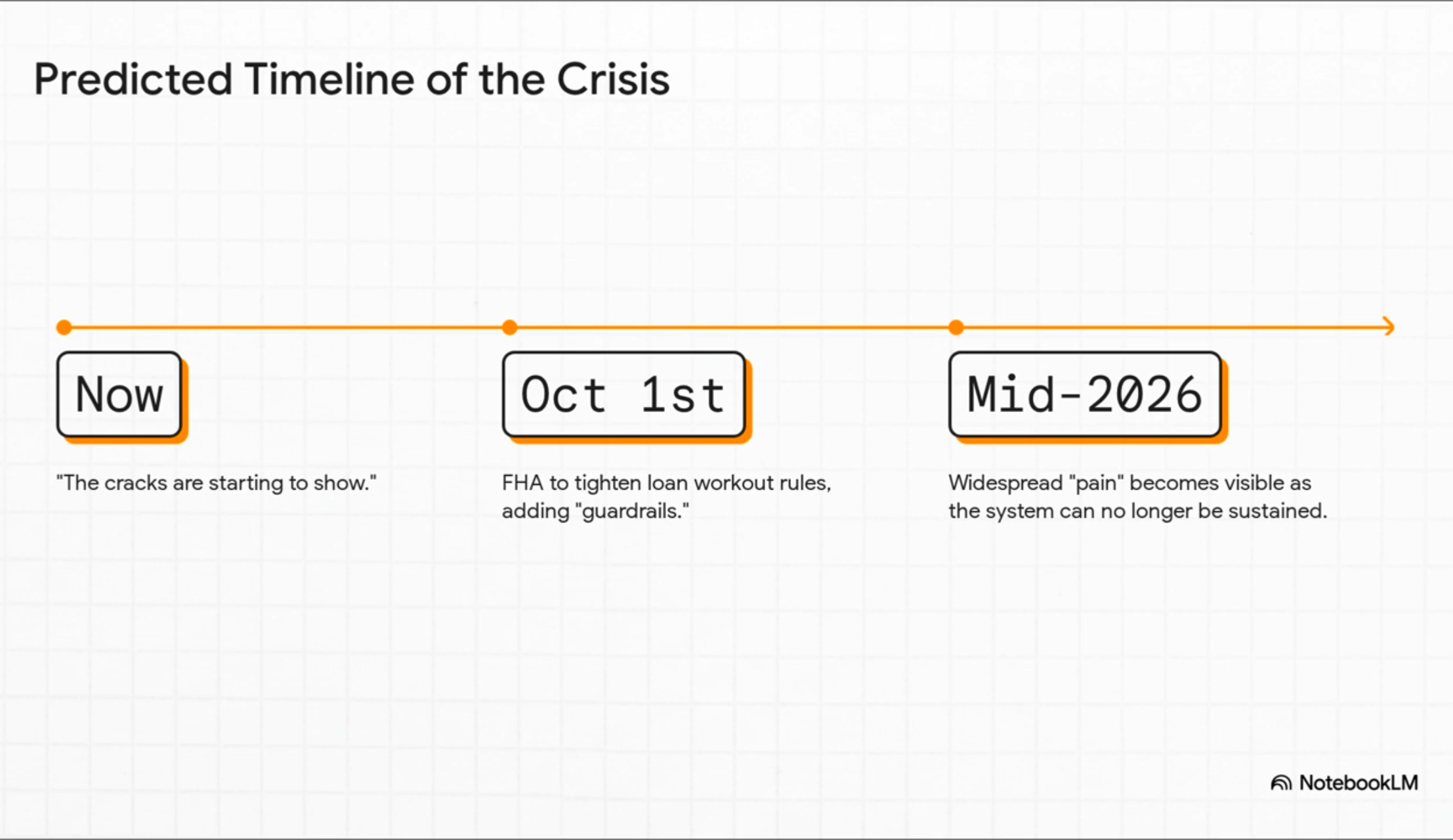

Mid to Late Next Year: "I've been saying for the last 6 months middle of next year is when you're going to see the pain middle of next year late mid to late next year That's when you're gonna really start seeing craters coming up all over the place."

October 1st FHA Changes: While largely unreported, new "guardrails" for FHA loans taking effect October 1st (limiting workouts to one per borrower) are expected to have a delayed but significant impact on foreclosures. "You're only going to get one workout after October 1st." This won't show up in headlines for a year.

"Running Out of Rabbits": The government is "running out of rabbits to pull out of their hat to keep this thing moving." The system's reliance on ever-increasing equity is unsustainable as values begin to fall.

Recommendations/Actionable Advice:

For Sellers: "If you want to sell get it priced right and get rid of it now Don't mess around." The market is "changing quarterly," and waiting for lower rates in the spring is ill-advised as prices are likely to continue to decline.

For Buyers: This period presents an opportunity. "If you're a home buyer this is actually good news for you you should be definitely getting prepared to strike while the iron's hot." Look for homes from sellers who have held property for 10-15 years (likely have equity) to negotiate on price, repairs, and closing costs. Aim to "buy at a next year price."

Increased Due Diligence: Be aware of the manipulated market data and economic indicators. Rely on personal financial observations rather than official narratives. "You don't have to listen to what they're saying in the news You don't have to listen to the politicians All you have to do is look at your own checkbook look at your you know your in your pocket Look at how expensive things cost."

Conclusion:

The housing market is facing a significant, yet largely concealed, crisis. The current stability is an illusion maintained by government intervention and artificial support, particularly through repeated loan modifications and the offloading of delinquent loans to private investors. As these "cracks" widen and the underlying affordability issues persist, a substantial market correction is anticipated in the coming year, with "pain" becoming widely apparent. The speakers emphasize that the fundamental problem is "ridiculous prices," which must come down, regardless of interest rate fluctuations.