A transcript unlocks clips, previews, and editing.

NVIDIA Circular Vendor Financing | It doesn't matter until it does

Featuring Anthony Scilipoti, forensic accountant who called the collapses of both Valeant Pharmaceuticals and Nortel before they happened.

Oct 30, 2025

I want to highlight that the content you should focus on is the interview of Anthony below on the The Knowledge Project Podcast. I have included both the podcast and YouTube formats for your pleasure.

The video companion at the top of the page is an AI NotebookLM generated summary with a 7 min runtime, if you do not have 93 minutes to listen to the entire interview.

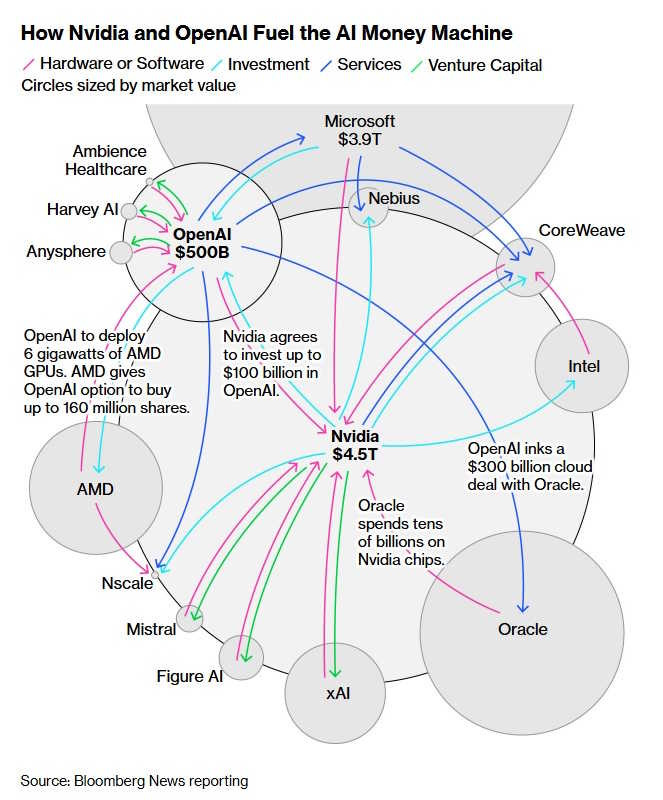

We have all seen the diagram by Bloomberg on the current AI circle jerk.

(Update Oct 30 8:51am NY)

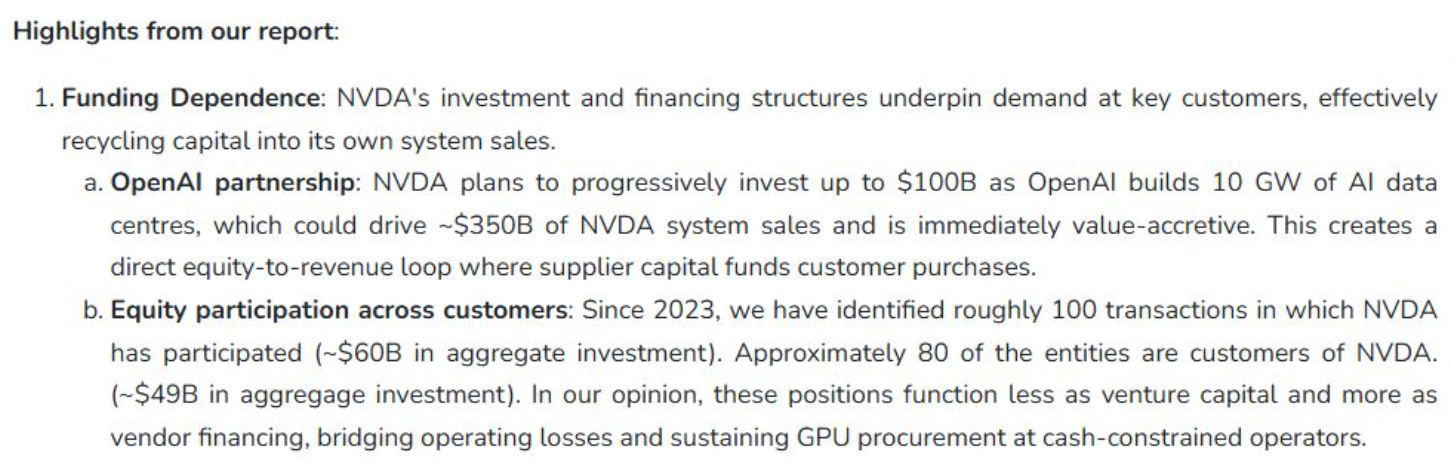

Everyone has heard of Nvidia’s circular transactions with OpenAI. At Veritas Investment Research, we have identified another 80-100 circular deals of Nvidia’s.

Our Special Situations Analyst Ben Butler, CFA, CPA Butler has done some great digging on Nvidia (see the snapshot below from his report to our clients a few days ago), continuing some of the work we’ve done on its circular transactions and accounting in the AI industry over the past three years. We concluded that the circularity of cash flows is now more material, more widespread, and much more conspicuous.

In my view, few investors are looking closely at NVDA’s accounting because it is all about growth. For the accountants out there, let’s just say that ASC606 and ASC323 may get in the way of growth expectations. If you know me, you know I’ve said this before - Nothing matters until it matters and when it matters, it matters a lot.

I won’t give too much away but my summary is simple. No one wants to be the party pooper while everyone is making money, and everyone’s making money. There are many components present that are very similar to Nortel and the networking expansion days of the dot com bubble. Anthony is not calling for a crash. He is simply pointing to the climate (windy conditions) we are in, and the flammable components (dry vegetation) present in the AI vendor financing merry go round.

The Coming Collapse? Insights from Forensic Accountant Anthony Scilipoti

Executive Summary

This document synthesizes the core insights and warnings from forensic accountant Anthony Scilipoti regarding the current state of equity markets, the AI boom, and the enduring principles of financial analysis. Scilipoti, who previously predicted the collapses of Nortel and Valiant Pharmaceuticals, identifies a period of “extreme euphoria” where investors dismiss fundamentals, echoing the dot-com bubble. The central argument is that while risk in the market is exceptionally high, it is being priced at historically low levels, evidenced by the tightest high-yield bond spreads and a benign VIX.

A key focus is the AI sector, where Scilipoti sees familiar warning signs of circular financing and investment structures reminiscent of the Nortel era. Companies like Nvidia and Microsoft are investing in their own customers (e.g., OpenAI, CoreWeave), creating an interconnected and potentially fragile ecosystem where sales growth is fueled by their own capital. These intricate relationships often lack full transparency, as individual transactions may not be material enough to warrant detailed disclosure for corporate giants.

Scilipoti is highly critical of the reliance on AI for financial analysis, framing it as a tool that accelerates information retrieval but cannot replace human judgment, experience, or the ability to form “mental models.” He warns that over-reliance on AI risks creating a generation of analysts who know the numbers but not what they mean.

To navigate this environment, he advocates a forensic accounting framework centered on identifying “flammable items”—potentially concerning data points—and waiting for a “spark” that turns them into genuine risks. This approach demands a deep, contextual understanding of a business, beginning with a thorough reading of financial statement footnotes to comprehend the accounting choices management has made. Ultimately, Scilipoti cautions that many of the forces at play—passive investing, retail investor influence, and flawed incentive structures—are creating a market vulnerable to a significant downturn when the prevailing narrative shifts.

Scilipoti characterizes the current equity market as being in a state of “extreme euphoria,” drawing direct parallels to previous bubbles where narrative has superseded financial fundamentals.

Comparison to the Dot-Com Bubble

The prevailing sentiment that “the numbers don’t matter and the financial statements no longer matter because this is changing the world” is a direct echo of the dot-com era.

Historical Precedent: Scilipoti recalls similar arguments made about companies like Nortel, Lucent, and Cisco, which were building the foundational infrastructure of the internet. While the internet did change the world, many of these foundational companies went bankrupt or were folded into others, and their stock valuations never recovered.

The Narrative Trap: Investors are being sold a “dream” about the future potential of AI, which makes them willing to overlook weak or non-existent current fundamentals, such as negative free cash flow and valuations based on revenue multiples.

Indicators of Mispriced Risk

A central thesis is that market risk is highest when the cost of that risk is priced at its lowest.

High-Yield Bond Spreads: The spread between the 10-year government bond and high-yield (non-investment grade) corporate bonds is near the tightest it has ever been. This indicates that investors are demanding very little extra compensation for lending to risky companies.

Low Volatility: The VIX, a measure of S&P 500 volatility, is trading at a “benign level,” signaling a broad market expectation of stability.

Scilipoti’s Conclusion: “The reason why I think we’re in a in a very high-risk situation is because the cost of the risk is priced very low and that’s when the risk is highest.”

The Economic Disconnect

There is a significant and concerning disconnect between all-time high market valuations and the financial health of the average consumer.

Consumer Strain: Major consumer-facing companies are showing signs of stress. Walmart has warned on sales forecasts, Target is struggling, Lululemon’s sales are slowing, and Starbucks is reconsidering its pricing and business model.

“Joe Sixpack” is Struggling: These data points suggest that the average consumer is facing financial pressure, which will ultimately impact corporate growth across the economy.

A Contrarian Indicator: The fact that Warren Buffett has built up his largest-ever cash holding at Berkshire Hathaway is noted as a significant indicator that the world’s most successful investor sees a lack of value in the current market.

II. The AI Boom: Echoes of Past Bubbles

While acknowledging AI as a transformative technology, Scilipoti warns that the financial structures supporting the boom are exhibiting the same dangerous patterns seen 25 years ago.

Circular Investment and Revenue Streams

A key “flammable item” is the circular flow of capital, where industry leaders invest in their own suppliers and customers, creating an illusion of organic growth.

The Microsoft/Nvidia/OpenAI Example:

Microsoft and Nvidia are investors in OpenAI.

OpenAI is a major customer of Microsoft’s cloud services and Nvidia’s chips.

Essentially, capital provided by Microsoft and Nvidia is cycled back to them as revenue from OpenAI.

The CoreWeave Example:

CoreWeave is a data farm whose largest customer is Microsoft.

Nvidia is CoreWeave’s primary chip supplier and is also a significant investor.

Nvidia made a last-minute $250 million investment to ensure CoreWeave’s IPO financing could close. The deal was underwritten by JP Morgan, which had also provided a pre-IPO loan to CoreWeave.

Nortel Parallels: This mirrors the dot-com era, when Nortel and Lucent would provide vendor financing and lines of credit to their customers. This propped up sales until the equity markets turned, at which point customers defaulted and the “wheels came off.”

The Problem of Disclosure and Accounting

Current accounting and disclosure rules may fail to capture the systemic risk building from these interconnected relationships.

Materiality Thresholds: An investment like Nvidia’s in CoreWeave is immaterial to Nvidia’s massive balance sheet, so it does not trigger significant disclosure requirements. The risk is not in a single transaction but in the aggregate effect of potentially hundreds of similar deals across the sector.

Accounting Manipulation: In the Nortel case, long-term receivables from customers were not classified as current assets or factored into operating cash flow, making liquidity and cash generation appear stronger than they were. After the collapse, accounting rules (FASB) were changed to correct this.

III. The Limitations of AI in Financial Analysis

Scilipoti argues that while AI is a powerful tool, its widespread adoption in finance is creating a dangerous gap in critical thinking and experience.

AI as an Accelerator, Not a Thinker

AI excels at information retrieval but lacks the capacity for judgment, context, and synthesis.

Functionality: AI can instantly find all references to a term like “capitalized interest” in a 300-page annual report, a task that once took a junior analyst hours.

The Limitation: It cannot understand the linkages between that data point and other notes, the cash flow statement, and the company’s business model. It lacks the ability to assess second and third-order consequences.

The Calculator Analogy: “You’re not going to use the calculator you need to learn it without the calculator and then you can use the calculator which is the same with AI. You need to understand how the financial statements are prepared understand the linkages develop mental models so that when the AI gives you information you can digest it and make decisions.”

The Experience and Judgment Gap

Over-reliance on AI risks stunting the development of the very skills that define a great analyst.

Hollowing Out the Junior Ranks: AI is replacing the foundational, “in the weeds” work where analysts learn the connections between financial statements and business reality.

The Chef Analogy: An AI user is like someone following a recipe—the result is good if conditions are perfect. An experienced analyst is like a chef—they understand the underlying principles and know how to diagnose and fix a problem when something goes wrong.

Knowing What Numbers Mean: The discussion references a conversation with Steve Schwarzman, who noted that many upcoming analysts “know the numbers but they don’t know what the numbers mean.” Experience is what teaches judgment.

IV. Principles of Forensic Accounting

Scilipoti outlines an analytical framework designed to identify genuine risk by combining deep financial analysis with an understanding of business context and human behavior.

Framework: Flammable Items and Sparks

This three-stage process moves beyond simplistic “red flags” to a more nuanced view of risk assessment.

Understand the Business & Control Environment: Analyze the business model, life cycle stage, management compensation, and, crucially, the specific accounting choices the company has made.

Identify Flammable Items: These are data points that are potentially concerning but not inherently negative on their own. For example, a company generating negative cash flow is a flammable item. If it’s a startup with a high return on invested capital, it may be a positive sign of investment.

Look for a Spark: A spark is a catalyst that makes a flammable item dangerous. For the negative cash flow company, a spark could be the entry of a new competitor or a rise in the cost of its debt, which threatens its entire model.

The Primacy of Financial Statement Footnotes

The notes are the most critical part of a financial report because they provide the context for interpreting the numbers.

Rule: “Read the notes to the financial statements first before you actually read the statements.”

Revealing Accounting Choices: The notes explain how management chose to account for various transactions. Accounting is a language, and the notes are the grammar key.

Historical Example: Enron’s catastrophic off-balance sheet exposures were not on the balance sheet itself but were disclosed in the notes, which very few people read.

Key Metrics and Their Pitfalls

EBITDA: Labeled “the mother of all disastrous measures” because it is easily manipulated and frequently misunderstood by investors as a proxy for cash flow. What constitutes an “add-back” is at management’s discretion.

Free Cash Flow (FCF): The standard formula (Operating Cash Flow - Capex) is often insufficient. The calculation must be adapted to the company’s business model.

Non-GAAP Metrics: A “huge flammable item” arises when a company changes how it calculates a custom metric like “adjusted EBITDA” from one year to the next. Valiant Pharmaceuticals was notorious for this practice.

V. Corporate Governance and Investor Behavior

Human factors, from management incentives to investor psychology, are critical drivers of both corporate success and failure.

Management Incentives and Trust

Rule: “Don’t Trust Management.” This is not an accusation of dishonesty but a professional mindset. The goal is to remain curious and skeptical, to “verify and then trust.”

Stock Options: These are heavily criticized for incentivizing short-term stock price movements, which management only partially controls. This can lead to decisions that are not in the long-term interest of the business. Share buybacks are often used primarily to offset the share dilution caused by stock options.

Incentive Consistency: A major warning sign is when a board changes the performance metrics for a management bonus after the fact because the original targets were not met.

The Psychology of Investing

Price Creates Narrative: As a stock’s price rises, its story becomes more believable and harder to question, regardless of underlying flaws. This was a key factor in how so many sophisticated investors were drawn into Valiant.

Bull Market Handicap: “During raging bull markets knowledge is superfluous and experience is a handicap.” Experience with past crashes makes an investor cautious, which leads to underperformance and pressure from clients.

Agency Problems: The structure of the money management industry forces a short-term focus. Portfolio managers who underperform a rallying market risk losing their clients, making it nearly impossible to hold a contrarian view for long. This is why Buffett, with his permanent capital base, is structured to act when others cannot.

Key Investing Rules Mentioned

Rule

Description

Avoid Embarrassing Loss

A modification of Buffett’s “don’t lose money.” The goal is to avoid catastrophic, portfolio-destroying losses (e.g., -50%), which allows for the intelligent absorption of calculated risks necessary for returns.

Emotion Has No Place in Investing

Decisions must be based on facts and analysis, not fear or greed.

Don’t Trust Management

Maintain a mindset of professional skepticism. Verify all claims before trusting them.

Read the Notes First

The footnotes to the financial statements must be read before the main statements to understand the accounting choices that shape the numbers.

Study Guide: Forensic Accounting and Market Analysis with Anthony Scilipoti

This guide is designed to review the key concepts, historical examples, and analytical frameworks discussed in the podcast featuring forensic accountant Anthony Scilipoti.

Quiz

Answer each of the following questions in 2-3 sentences, based on the information provided in the source context.

What is Anthony Scilipoti’s three-stage process for forensic analysis, and how does he differentiate it from simply looking for “red flags”?

According to the transcript, what were the “off-balance sheet exposures” that led to Enron’s collapse?

How does Scilipoti argue that AI can exacerbate problems for investors who do not fundamentally understand financial statements?

What specific parallel does Scilipoti draw between the business practices of Nortel during the dot-com era and major AI companies today?

What two market indicators does Scilipoti cite to argue that the cost of risk is currently priced “very low”?

Explain Scilipoti’s distinction between a “flammable item” and a “spark” using the example of a company with negative cash flow.

According to the discussion, why did many well-respected investors fail to see the problems at Valiant Pharmaceuticals?

What is Scilipoti’s number one investing rule, and how does it modify Warren Buffett’s famous rule?

Why does Scilipoti refer to EBITDA as the “mother of all disastrous measures”?

What is Scilipoti’s primary argument for why stock options should be treated as an expense and are often a poor incentive for employees?

Answer Key

Scilipoti uses a three-stage process involving: 1) understanding the business, control environment, and accounting; 2) identifying “flammable items” which are potential issues that are not inherently problematic; and 3) looking for a “spark,” or a catalyst that turns a flammable item into a major problem. This is different from looking for “red flags,” which can lead to prematurely dismissing a company without understanding the full context.

Enron had numerous derivative contracts tied to energy prices or its own stock price that were contingent and not listed as liabilities on its balance sheet. When a recession in the early 2000s caused commodity prices to move, these derivatives were triggered, and Enron was unable to make the required payments, leading to its rapid collapse.

Scilipoti argues that while AI can quickly pull references from financial documents, it lacks the judgment to understand the linkages and second-order consequences between data points. Investors who rely on AI without first developing their own mental models and understanding of accounting may get information without the context needed to make a sound decision.

Scilipoti points to circular investment patterns as a key parallel. Just as Nortel would provide financing to its own customers, he observes that today’s major AI players like Nvidia and Microsoft are investing in their own customers and suppliers (e.g., OpenAI, CoreWeave), creating an interconnected and potentially fragile ecosystem.

He points to the high yield bond spread (the difference between the 10-year government bond and non-investment grade bonds), which is near its tightest level in history. He also cites the VIX (a measure of S&P 500 volatility), which is trading at a “benign level,” indicating that investors in both bond and equity markets are not pricing in significant risk.

A flammable item is a condition that is not problematic on its own, such as a company generating negative cash flow while investing for high-return growth. A spark is an external event that makes the flammable item dangerous, such as a new competitor entering the market, which could threaten the company’s future growth and make its negative cash flow and debt load a critical issue.

Many respected investors were misled by Valiant because its CEO, Mike Pearson, was a “masterful spinner of a story” and the company’s stock price kept rising, which created a powerful narrative of success. This phenomenon, where “price creates narrative,” makes it incredibly difficult for money managers to stay the course on a negative view when they are underperforming the market.

Scilipoti modifies Warren Buffett’s rule “don’t lose money” to “avoid embarrassing loss.” He argues that all investing requires taking on some risk of loss, but investors must avoid catastrophic losses (e.g., a 50% drop) from which a portfolio, and an investor’s reputation, cannot easily recover.

He considers EBITDA a disastrous measure because investors mistakenly believe it represents cash flow when it is purely an operating performance metric. Furthermore, it is a non-GAAP metric that management can manipulate by excluding various costs (like stock options or acquisition charges) to present a misleadingly positive picture of performance.

Scilipoti argues stock options should be an expense because they are a form of payment, just like cash. He also believes they are a poor incentive because an employee’s compensation becomes tied to the stock price, which can be influenced by many external factors (like Fed policy or GDP data) that the employee has no control over.

Essay Questions

The following questions are designed for longer, more analytical responses. No answers are provided.

Drawing from Scilipoti’s discussion on AI, experience, and mental models, analyze the argument that human judgment remains critical in financial analysis despite technological advancements. Use the “chef’s recipe” analogy from the transcript to support the analysis.

Discuss the cyclical nature of market euphoria as described by Anthony Scilipoti. Compare and contrast the “symptoms” he identifies in the dot-com bubble (Nortel, Lucent) with those he sees in today’s AI-driven market, focusing on circular investments and accounting interpretations.

Explain the concept of “price creates narrative” using the Valiant Pharmaceuticals case as a primary example. How does this phenomenon, combined with pressure on money managers to perform, create an environment where flawed companies can thrive for extended periods?

Scilipoti outlines three key factors that influence accounting decisions: facts, constraints, and objectives. Using examples from the text (like Nortel’s long-term receivables or a hypothetical company wanting to sell its business), explain how these three factors interact to shape a company’s financial statements.

Analyze the structural issues within the modern investment landscape that Scilipoti discusses, including the rise of passive investing, the increased power of retail investors, and the agency problems faced by professional money managers. How do these factors contribute to market volatility and a short-term focus?

Glossary of Key Terms

Term

Definition from Source Context

Forensic Accountant

An accountant who performs due diligence and in-depth analysis of transactions and financial statements to find concerns with the accounting. The work goes beyond standard audits to investigate the underlying reality of a company’s financial position.

Flammable Items

Potential issues within a company’s financials or business model that are not inherently negative on their own but could become problematic under certain conditions. For example, negative cash flow is a flammable item, not a definitive “red flag.”

Spark (in forensic accounting)

A catalyst or event that turns a “flammable item” into a significant problem. For instance, the arrival of a new competitor could be the spark that makes a company’s high debt and negative cash flow unsustainable.

Off-Balance Sheet Exposures

Financial risks or liabilities, such as derivative contracts, that are not included on a company’s main balance sheet under prevailing accounting rules. Enron used these to hide its true level of risk from investors.

Fundamentals (Scilipoti’s Definition)

The process of forecasting a company’s future cash flows to determine its present value. This is contrasted with other definitions that may focus on chart patterns, technical indicators, or simple earnings multiples.

High Yield Bond Spread

The difference in interest rates between the 10-year U.S. government bond and non-investment grade (”high yield” or “junk”) bonds. A tight spread indicates that investors are not demanding much extra compensation for lending to risky companies.

VIX

A measure of the market’s expectation of volatility in the S&P 500. A “benign” or low level indicates that investors perceive low risk in the equity market.

Free Cash Flow

Traditionally defined as operating cash flow less capital expenditures (capex). Scilipoti argues this simple formula is flawed and must be adapted to the company’s business model, industry, and life cycle, citing how Nortel’s long-term receivables should have been included.

EBITDA

Earnings Before Interest, Tax, Depreciation, and Amortization. Scilipoti calls it a “disastrous” non-cash flow metric that is easily manipulated by management choosing what costs to include or exclude, leading investors to believe it represents cash.

Non-GAAP Metrics

Financial measures, such as “adjusted EBITDA,” that are not audited and are defined by management. Scilipoti warns that companies can change the calculation method from one year to the next to present results in the best possible light.

Stock Options (as an expense)

Scilipoti argues that if a company pays an employee with stock options instead of cash, it is still a form of compensation and should be treated as an expense. Not doing so artificially inflates metrics like EBITDA and EPS.

Passive / Index Investing

An investment strategy that involves buying a market-cap-weighted index (like the S&P 500). Scilipoti views this as a form of momentum investing because new money flows disproportionately to the largest companies, pushing their prices higher.

Price Creates Narrative

The phenomenon where a rising stock price itself becomes the justification for a company’s success, causing investors to overlook underlying fundamental flaws. This was a key factor in the long-term success of Valiant’s stock before its collapse.

Agency Issues (in money management)

The conflict that arises because professional money managers are measured on short-term performance relative to a benchmark. This pressure from their clients (the principals) can force them to abandon sound, long-term theses and buy into overvalued trends to avoid underperforming.

Circular Investments

A pattern where a company invests in its own customers or suppliers, creating a self-reinforcing loop of revenue and investment. For example, Nvidia investing in CoreWeave, which is a major buyer of Nvidia’s chips.

Discussion about this video

Not Your Advisor

Daily Stock Markets coverage in under 15 min. No ads. No politics! Easy to follow for your morning coffee, dog walk or commute.

For free subscribers, you can unlock everything for 7 days free: https://www.notyouradvisor.com/unlock

What you get with the upgrade

Unlocked full daily podcast episodes

Premium only Stock Spotlights

Break out and breakdown watchlists

Concierge intraday alerts and private group chatroom

Member Chart requests

Full archive 500+ written and 500+ podcasts!

Educational content to learn how to read the markets using breadth, macro and technical analysis through the lens of Auction Market Principles

Recently a paying subscriber noted in the private group chat he has begun booking 300% gains on PLTR from less than a year ago, when I alerted about its break out setup in the $20s, $30s.

But please note, I am not offering a stock picking service! While many of the ideas went up 30%, 50%, 100%, and 800%+, my goal is to help others find setups on their own and obtain a unique lens into observing and analyzing the global markets. Once you see it, you cannot unsee it.

This will not be easy! There are no magic signals to upload to your charting software or promises of turning $1000 into $100k. It will require work, objectivity, and self knowledge.

“Remember, all I'm offering is the truth. Nothing more”

Highlights

Recommended by investors who are trying to learn how to read the markets in a way Wall St doesn't want us to see them.

Daily podcast of the stock market in 15 minutes. No advertising No politics!

Great content for young investors getting started or those who simply want the skills to grade their financial advisors work

Watch lists of bullish and bearish setups

Frequent stock spotlights

Private trading room with intraday play by play and alerts

Substack Featured 3 times and a Best Seller with thousands of free subscribers and hundreds of happy paying subscribers

Recommended by

Doomberg

Adam Taggart

John Rubino

Herb Greenberg

and many others

Subscribers include:

Executives at Fortune 100 companies

Novice investors

Financial professionals

Soon-to-be retirees

Testimonials

“Thank you so much for everything you have taught me. I don't talk much anymore since I am busy watching charts and doing everything you taught with the breakouts and volume and stops. I hit my all time high today in the market! Some was recovery but much was from my day trading and scalping for extra money.”

- JRoth (Paying Subscriber)

"As a subscriber for nearly a year I had the opportunity to experience your thought process. Invaluable. No nonsense. No guesswork. The amount of data is crunched every day is obvious from the podcasts! The chat room is connected to the pulse of the market. Full of trading ideas and I can find my own ways too. In fact, NYUGrad is giving tools and freedom, not advice! PRO"

- Turbolaser Whack (Paying Subscriber)

"Your ability to put snaps of the market together are extraordinary. I spend most of my time in the futures markets but you are one profile that everyone could use. Succinct and chocked full with info that is USABLE - you rock."

- Anne-Marie Baiynd (Paying Subscriber)

Daily Stock Markets coverage in under 15 min. No ads. No politics! Easy to follow for your morning coffee, dog walk or commute.

For free subscribers, you can unlock everything for 7 days free: https://www.notyouradvisor.com/unlock

What you get with the upgrade

Unlocked full daily podcast episodes

Premium only Stock Spotlights

Break out and breakdown watchlists

Concierge intraday alerts and private group chatroom

Member Chart requests

Full archive 500+ written and 500+ podcasts!

Educational content to learn how to read the markets using breadth, macro and technical analysis through the lens of Auction Market Principles

Recently a paying subscriber noted in the private group chat he has begun booking 300% gains on PLTR from less than a year ago, when I alerted about its break out setup in the $20s, $30s.

But please note, I am not offering a stock picking service! While many of the ideas went up 30%, 50%, 100%, and 800%+, my goal is to help others find setups on their own and obtain a unique lens into observing and analyzing the global markets. Once you see it, you cannot unsee it.

This will not be easy! There are no magic signals to upload to your charting software or promises of turning $1000 into $100k. It will require work, objectivity, and self knowledge.

“Remember, all I'm offering is the truth. Nothing more”

Highlights

Recommended by investors who are trying to learn how to read the markets in a way Wall St doesn't want us to see them.

Daily podcast of the stock market in 15 minutes. No advertising No politics!

Great content for young investors getting started or those who simply want the skills to grade their financial advisors work

Watch lists of bullish and bearish setups

Frequent stock spotlights

Private trading room with intraday play by play and alerts

Substack Featured 3 times and a Best Seller with thousands of free subscribers and hundreds of happy paying subscribers

Recommended by

Doomberg

Adam Taggart

John Rubino

Herb Greenberg

and many others

Subscribers include:

Executives at Fortune 100 companies

Novice investors

Financial professionals

Soon-to-be retirees

Testimonials

“Thank you so much for everything you have taught me. I don't talk much anymore since I am busy watching charts and doing everything you taught with the breakouts and volume and stops. I hit my all time high today in the market! Some was recovery but much was from my day trading and scalping for extra money.”

- JRoth (Paying Subscriber)

"As a subscriber for nearly a year I had the opportunity to experience your thought process. Invaluable. No nonsense. No guesswork. The amount of data is crunched every day is obvious from the podcasts! The chat room is connected to the pulse of the market. Full of trading ideas and I can find my own ways too. In fact, NYUGrad is giving tools and freedom, not advice! PRO"

- Turbolaser Whack (Paying Subscriber)

"Your ability to put snaps of the market together are extraordinary. I spend most of my time in the futures markets but you are one profile that everyone could use. Succinct and chocked full with info that is USABLE - you rock."

- Anne-Marie Baiynd (Paying Subscriber)